Predictive models, one per coin, watch the crypto order book and candles and

emit a buy/sell confidence every second. This page follows the whole pipeline

— from the raw market firehose to live orders on Binance — and ends

on the bot’s live read, this second.

checking feed…

Live

Running right now

Everything above describes a system that is, as you read this, watching the

market. Below is its live output: for each coin, the model’s buy

confidence this second, against the threshold it must clear to act. When a bar

crosses its threshold, that is the bot deciding to enter.

Live · 5 coins from Hetzner

connecting to the feed…

Bar = buy confidence (0–1). The notch is the per-coin threshold;

a bar past the notch turns crimson — the bot would enter. Arrow shows

the last price tick’s direction.

The trajectory, coin by coin

The ticker is the snapshot; this is the path. Each dot is one prediction,

plotted as the price the model saw against the confidence it produced —

so you can watch a coin walk toward, or away from, its threshold over time.

Live · price × confidence

Connecting…

—

Each dot is one second’s prediction. The trajectory walks through price (x)

against the model’s buy confidence (y). The dashed line is the buy threshold —

points above it trigger the bot. Select multiple coins to compare confidence trajectories.

The firehose from Act 1 is still flowing. The candles are still forming, the

features still computing, the model still scoring. Everything on this page is

one continuous loop — and the numbers above are its read on the market,

this second.

§

A crypto market never stops talking. Every second, for every coin, it emits

a fresh burst of numbers — the last trades, the shape of the order

book, who is leaning to buy and who to sell. On its own that stream is

noise: too fast to read, too wide to hold in your head.

This is the story of the machine that turns that noise into a decision. It

runs continuously on a box in a German datacentre, collecting the firehose,

folding it into candles, computing close to two hundred features a second,

training and scoring models, and — when one is confident enough —

placing a real order on Binance. No background assumed: we build it up one

stage at a time, each shown with the production artifact rather than a

mock-up.

What this demonstrates

End-to-end ML system — data pipeline, training, model selection, live execution

Real-time engineering — a per-second firehose folded into ~190 features

MLOps discipline — every run tracked in MLflow, reproducible not vibes

Live in production — placing real orders on Binance right now

Every sample on this page is real, captured from the production system:

the raw rows and k-lines come straight off the live collector (their

timestamps are genuine Unix seconds), the architecture diagram and MLflow

and Binance screenshots are the system’s own, and the final feed is

live. Where a feature illustration needed a longer history than the short

samples carry, it is drawn schematically and labelled

illustrative — never fabricated numbers.

§

Act 01

The firehose

Start where the system starts: with what one coin actually looks like before

anyone has interpreted it. The collector wakes up every second, asks Binance

for the latest trades and the current order book, and writes a single row.

Here are three of those rows for ETH.

symbol

ts_begin

ts_end

open

low

high

close

wavg

volume

trades

twb0.3%

tws0.3%

twb1%

tws1%

eth

1780050104

1780050164

2010.35

2010.25

2010.87

2010.74

2010.5865

28.7425

129

692.631

820.6453

930.3267

1032.9208

eth

1780050105

1780050165

2010.35

2010.25

2010.87

2010.55

2010.6003

31.5912

137

692.631

820.6453

930.3267

1032.9208

eth

1780050165

1780050166

2010.55

2010.55

2010.55

2010.55

2010.55

0

0

688.9162

839.4716

928.0666

1050.0721

189 columns per row, about one row per second, per coin, 24/7.

You are seeing the first 14 columns of 3 rows — the other 175 keep

scrolling off to the right. Scroll the panel to feel the width.

The first ten columns are the familiar stuff: the symbol, the time bucket

(ts_begin / ts_end as

Unix seconds), open/low/high/close prices, a volume-weighted average price,

the traded volume and the number of trades. Then it gets more interesting:

the twb/tws columns are

trade-weighted order-book depth — how much buy and sell

liquidity sits within 0.3%, 1%, 3% and 10% of the mid-price. And those fourteen

are just the beginning: another ~170 derived indicators are appended to every

single row.

Where this came from

These are unedited rows captured from the production collector running on a

Hetzner box. The timestamps are real Unix seconds; the third row is a

one-second bucket with a single trade, which is why its open, high, low and

close all collapse to the same price and its volume is zero.

No human reads this. No model trains on it directly either — it is too

fast and too raw. The first thing the system does is fold time into something

a person, and a model, can actually hold: candles.

A market emits noise a thousand times a second. The rest of this page is how

that noise becomes a trade.

§

Act 02

Folding time into candles

The first transformation is the oldest trick in market data: stop looking at

every tick, and summarise each minute by four numbers — where it opened,

how high it went, how low, and where it closed. A candle.

Below are eight consecutive one-minute candles for ETH, aggregated from the

same raw stream.

time

open

high

low

close

volume

trades

OB buy 1%

OB sell 1%

18:34

3832.51

3833.99

3832.50

3833.99

33.46

177

2,043

3,087

18:35

3833.98

3833.99

3829.39

3829.39

228.61

492

2,737

3,733

18:36

3829.40

3829.40

3822.58

3822.59

549.02

1,117

2,615

3,725

18:37

3822.59

3823.60

3793.00

3799.67

5867.46

14,016

2,213

3,666

18:38

3799.67

3799.84

3788.32

3795.20

2345.27

5,194

2,012

3,375

18:39

3795.20

3795.76

3789.96

3793.63

1087.61

1,778

2,107

3,495

18:40

3793.63

3794.52

3776.00

3784.72

3291.32

7,062

2,166

3,865

18:41

3784.72

3793.33

3784.72

3790.30

1408.17

2,160

2,008

3,045

Eight one-minute k-lines for ETH (times UTC). Open / high /

low / close, plus volume, trade count, and order-book buy & sell depth

within 1% of mid-price — the microstructure carried through from the

raw feed.

Anatomy of one candle

Each row of that table is one of these. The thin line — the

wick — spans the highest and lowest price touched in the minute.

The thick body spans open to close. A filled body means the minute

closed higher than it opened; a hollow body means it closed lower.

The table, as a chart

Line those eight candles up in time and the table becomes something you can

read at a glance: a quiet open, then a sharp sell-off on the minute with

14,016 trades, then a tentative recovery.

Built from the rows above. Filled = closed up, hollow =

closed down; wick = high–low. Same eight rows, now legible as price action.

Candles are readable, but they are still just price. To predict, the

system needs to turn this shape — and the order-book depth riding

alongside it — into numbers that say something about what happens next.

That is feature engineering.

§

Act 03

Candles into signals

A candle tells you what just happened. A feature tries to say

something about what happens next. On top of every k-line the system computes

the full TA-Lib battery — roughly 180 indicators, including 61

candlestick-pattern detectors — and feeds them all to the models. Three

are worth seeing up close.

Order-book depth & imbalance — the edge

What it is: how much real buy versus sell liquidity is

resting within 0.3%, 1%, 3% and 10% of the mid-price — the

twb/tws columns from Act 1.

Why it predicts: price history is the past; the order book is

intent. A wall of bids just under the price tends to hold it up; a

wall of asks above tends to cap it. This is the least textbook of the three,

and the part that earns its keep.

Real depth, ETH @ 18:35 UTC. Right at the mid (±0.3%) buyers

dominate; a little further out (±1–3%) sellers stack up; far out (±10%) deep

bid support returns. The imbalance flips by band — exactly the

structure a model can learn from.

RSI(14) — momentum

What it is: the Relative Strength Index, a 0–100 gauge of

how one-sided recent moves have been. Above 70 is conventionally

“overbought,” below 30 “oversold.”

Why it predicts: streaks exhaust themselves. Stretched momentum

often precedes a pause or a snap-back, so RSI helps the model temper a signal

that is running hot.

Illustrative. When the oscillator pushes into the upper band,

price has run hot; the lower band marks oversold. Shape shown for intuition,

not computed from the eight-row sample.

Bollinger Bands — volatility

What it is: a moving average with an envelope drawn a couple of

standard deviations above and below it. The bands breathe with volatility.

Why it predicts: a tight squeeze means the market is coiled and

a breakout is likely; price riding the upper band signals strength, hugging the

lower band signals weakness.

Illustrative. The envelope starts tight (a squeeze) and

widens as volatility rises; the dashed centre line is the moving average.

…and 186 more

These three are a window, not the catalogue. The feature index runs to 189

columns — MACD, ATR, ADX, stochastics, on-balance volume, the 61

candlestick patterns, and the order-book depth/std bands — all computed

every second and handed to the models. The point of this act is the

idea: price and order book in, a wide vector of signals out.

So now there are ~189 numbers per second, per coin. What consumes them, turns

them into a buy/sell confidence, and decides when to act? That is the machine.

§

Act 04

The machine

Everything so far — the firehose, the candles, the features — is

feedstock. This is the machine it feeds. The diagram below is the system’s

own blueprint, recolored to match this page; it has two halves that meet at a

single object, the model.

The Bintri optimization architecture. Box colour encodes

node type (see legend): petrol = optimized, sand = artefact, clay = data or

process. View full size ↗

The left half — building a model

A historical dataset is narrowed by filters

(which coins, which times of day, how recent), producing the

filtered dataset that model training learns

from. Training also takes labels — derived from a forward

time window (did the price move enough, soon enough, to be

worth a trade?) — and a set of model parameters. The

candles from Act 2 and the ~189 features from Act 3 are exactly what flows in

here. Out comes a model, scored by a

recall/precision curve and a backtest over

held-out history.

The right half — trading it live

The grey Strategy box is the live loop. It holds a

threshold per coin (how confident the model must be to act),

an entry rule (what fraction of equity, after how many

seconds’ delay), and logic to evaluate open positions

for early closure. It consumes the latest k-lines in real

time, and when the model’s confidence clears the threshold it sizes a

position against the latest close / average fill price and

closes the loop into Binance — futures and shorts

included, trading fees accounted for.

On the “profit” boxes

The backtest profit and profit nodes in the diagram are the

system’s objective functions — what training and

the strategy are optimized toward — not a claim about realized

returns. The legend’s “optimized independently” versus

“optimized jointly” marks which parts are tuned in isolation and

which are searched together.

One box on the left hides an enormous amount of work: model

training. Choosing a good model means running it hundreds of times

over different features, windows and parameters. How do you keep that honest

and comparable?

§

Act 05

How models are chosen

“Train a model” is really “train a few hundred and keep the

best one.” Each run is a different combination of features, look-back and

forward windows, label definitions and hyper-parameters. The only way to choose

between them without fooling yourself is to log every run, identically, and

compare. That is what MLflow is for.

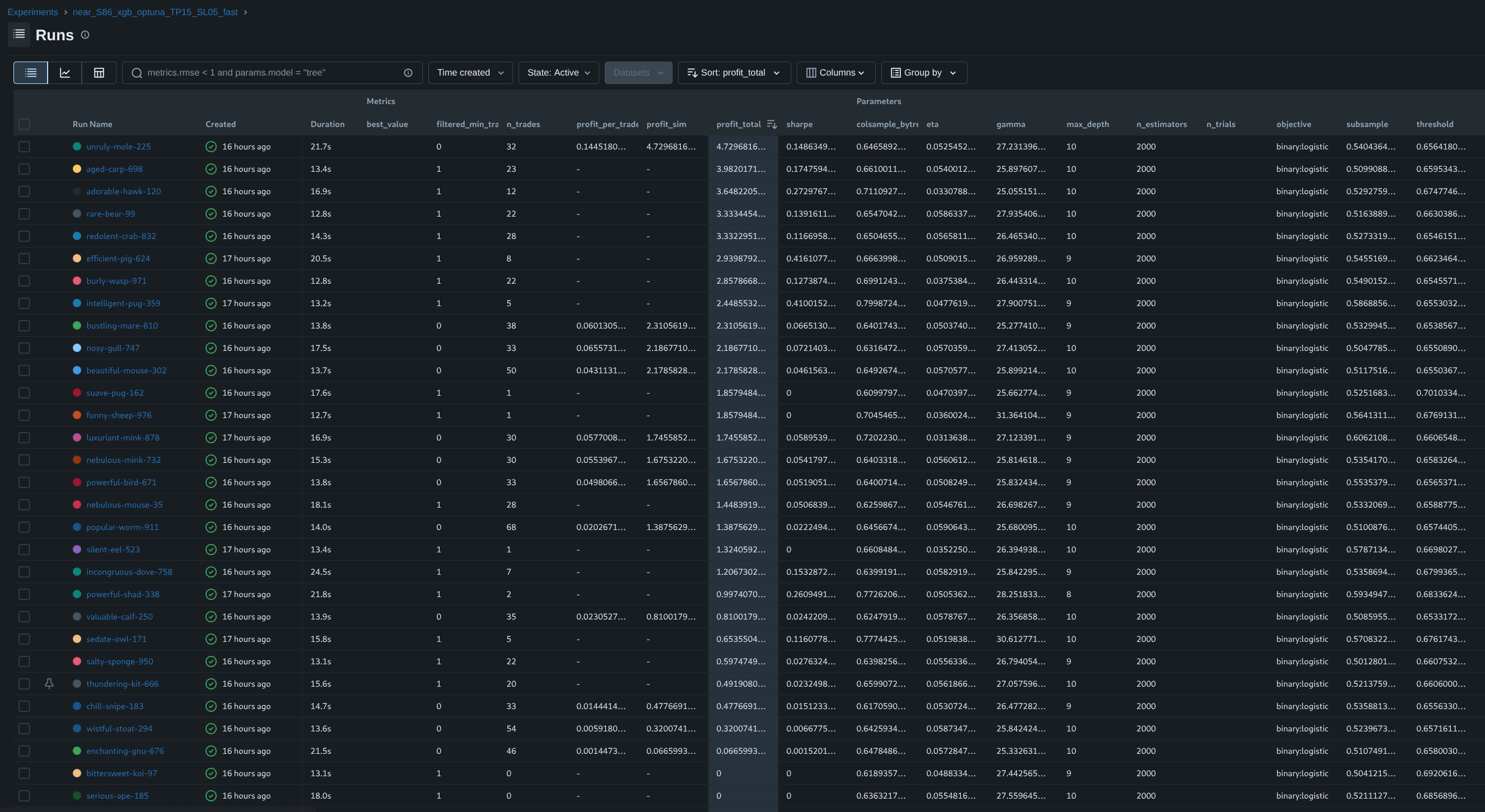

The MLflow runs table for the trading models. Every row is one

training run; every column a logged parameter or metric (precision, recall and

the rest), so runs line up for direct comparison.

View full size ↗

Each run records its parameters (what was tried), its

metrics (how it scored — the precision/recall numbers

behind that curve in Act 4), and its artifacts (the trained

model itself). Because the logging is uniform, model selection becomes a

sort-and-filter over a table rather than a matter of memory or vibes: you can

ask “best precision at a given recall” and get an answer you can

reproduce tomorrow.

The features from Act 3 are the raw material these runs consume; the winner is

the model that gets promoted into the live Strategy box from Act 4. Which means

it stops being a row in a table and starts doing something with real money.

§

Act 06

Live orders on Binance

When the selected model’s confidence clears a coin’s threshold, the

Strategy box does the thing all of this was for: it places an order. Not a

paper order — a real one, on the exchange, with the account’s own

funds. Here is a slice of that order history.

Executed orders on Binance. Each row is a real order the bot

placed — market and limit, buy and sell, across XRP and DOGE — with

its timestamp and fill price. View full size ↗

This screenshot is here to show one thing: the loop closes. Raw feed →

candles → features → a trained, selected model → a strategy → an order

that actually executes on a live exchange. It is not a performance

claim. The system is experimental and has no proven profitability track to

point at; what it has is a complete, working path from market noise to a real

trade.

Which leaves one last question, and the most fun one to answer live: what is

the model thinking right now?

§

Bonus

Get signals on Telegram

Don’t want to leave this page open? The same buy signals the system

produces are pushed to a Telegram bot the moment they cross the entry

threshold — so you can watch from your phone while the bot runs

on the server.

Subscribe to @Bintri_Alerts_bot

to receive a notification each time the model decides to enter a position

on any of the five tracked coins.

The current models are deliberately conservative: a buy signal is only

issued when the model’s confidence exceeds a per-coin threshold

that is rarely reached in normal market conditions. In practice, the

bot may go days without triggering a single entry. Silence is not a

prediction that prices will fall — it means the model does not

see a high-confidence setup.

Not investment advice

All signals generated by this system are shared for informational and

educational purposes only. They do not constitute financial advice, an

offer to buy or sell any asset, or a recommendation to trade.

Cryptocurrency markets are highly volatile; past performance is not

indicative of future results. Never invest more than you can afford to

lose.